Can RFK’s Government-Backed Mortgage Plan Be Feasible For New Home Buyers?

On October 1, 2023, Robert F. Kennedy, Jr. (“RFK”) announced a new economic plan as part of his presidential campaign, featuring a guaranteed government-backed mortgage at 3%. (Carlson, The Hill). RFK’s government-backed mortgage plan (the “Plan”) is intended to incentivize working-class Americans to buy more homes. (https://www.kennedy24.com/help-buying-homes-video). The Plan achieves this goal by providing low interest rates, which would be appealing to working-class citizens. Id. The overall issue that RFK is aiming to address with his Plan is to stop the current takeover of the housing market by investment companies and the consequent increasing housing prices. Id. This post discusses the potential conflict that RFK’s Plan could have with existing government-backed mortgages provided by government agencies, the Federal Trade Commission’s (“FTC”) mortgage regulations, and possible economic consequences on the housing and mortgage markets.

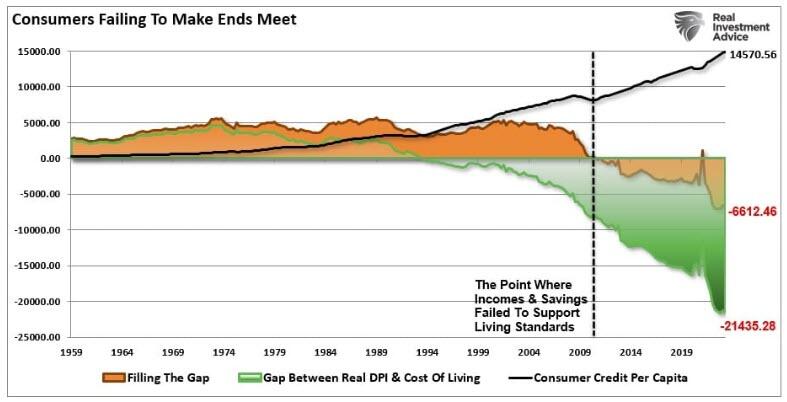

The shift of $4 trillion in wealth from the working class to the super wealthy in the United States since 2020 has heightened concerns when it comes to the housing market. (Carlson, The Hill). This shift, paired with annual wages $5,000 below the basic cost of human needs has caused a steady decline in homeownership following the 2008 housing crisis. (https://cms.zerohedge.com/s3/files/inline-images/2023-09-22_05-57-05.jpg?itok=X6xShiCB). Adding to the working class’s reluctance to purchase homes, is the average cost of a home rising to be over $400,000 since 2020. (Caporal, The Ascent). Additionally, the recent trend of large investment companies like BlackRock, State Street, and Vanguard acquiring significant portions of the housing market, with current projections indicating that 40% of all houses in the market will be owned by large companies by 2030, and build-to-rent houses, further threatens private home ownership. (Carlson, The Hill). As a result, RFK’s Plan has the potential to curb investment companies takeover of the housing market by encouraging working class citizens to buy houses by providing attractive interest rates. (https://www.kennedy24.com/help-buying-homes-video).

{kind=link}

The Federal Housing Administration (“FHA”), U.S. Department of Agriculture (“USDA”), and the Department of Veterans Affairs (“VA”) each have their own government backed mortgage programs. (Patoka, Forbes). The FHA loan is intended for low- and moderate-income home buyers, offering current interest rates around 7.4% and, and down payments currently as low as 3.5%. (LaPonsie, Forbes). The USDA loan, similar to the FHA loan, is intended for low- and moderate-income home buyers, however, this mortgage is for buyers in communities of 35,000 residents or smaller with the current interest rate being 7.6%. (Patoka, Forbes; and (https://www.usdaloans.com/program/rates/). The VA loan is for veterans and their spouses. Id. The VA mortgage loan varies and encompasses a wider range of buyers with the current interest rate for loan at 6.25%. (https://www.navyfederal.org/loans-cards/mortgage/mortgage-rates/va-loans.html). The bar to the qualify for RFK’s Plan would be relatively low since he has not provided the exact qualifications for the Plan yet, saying that this mortgage will apply to “millions of Americans”. https://www.kennedy24.com/help-buying-homes-video). RFK’s Plan threatens the FHA, USDA, and VA as it would apply to everyone who would be eligible for their loans and offers a lower interest rate of 3% compared to the interest rates of 7.4%, 7.6%, and 6.25% of the other government agency loans. (Carlson, The Hill) (LaPonsie, Forbes) (https://www.usdaloans.com/program/rates/) (https://www.navyfederal.org/loans-cards/mortgage/mortgage-rates/va-loans.html).

Despite the appeal of the Plan and benefit to lower income citizens, it may still face legal challenges. The FTC has enacted regulations on mortgages to prevent deceptive mortgage practices that could come into conflict with RFK’s Plan. (FTC). However, the FTC’s regulations on mortgages only apply to companies that are a “for-profit provider of mortgage assistance relief services”. (FTC). The FTC further defines this class as “a service, plan, or program that is represented, expressly or by implication, to help homeowners prevent or postpone foreclosure or help them get other kinds of relief, like loan modifications, forbearance agreements, short sales, deeds-in-lieu of foreclosure, or extensions of time to cure defaults or reinstate loans.” Id. It is debatable if the US government would fall under this class as it is not traditionally categorized as a “for-profit provider” but would satisfy the second part of the definition as a mortgage assistance relief service as it provides a service that is expressly provided to help homeowners. (https://www.kennedy24.com/help-buying-homes-video). Further, looking into the FTC’s regulations, one of the provisions is that the mortgage service would need to disclose that they are “not associated with the government”. (FTC). Since RFK’s Plan would come directly from the executive branch, this could mean that the mortgage plan is exempt from the FTC regulations. As a result, RFK’s Plan could not be regulated by the relevant government agencies, thus making it open to passing standards that might be illegal under the FTC.

If RFK’s Plan is enacted, it could cause banks to lessen their presence in the housing market. Since the 2008 housing crisis, banks provided fewer mortgages as people have been generally skeptical about taking out a mortgage. (Salmon, Axios). Additionally, as a result of banks paying more than $100 million in mortgage fines stemming from the housing crisis, banks have been more reluctant to provide mortgages. Id. Consequently, the mortgage market is currently dominated by non-bank entities – with 71% of agency-backed loans and 86% of government-backed loans originating from non-bank entities. Id. If RFK’s Plan is to become the inclusive plan that he is advertising, this would steal most clients from the banks as only a small amount of people who would not qualify for the Plan would result in taking a mortgage from a bank. (https://www.kennedy24.com/help-buying-homes-video). Given the additional component of a 3% interest rate in RFK’s Plan, it would be hard for the banks to compete with and could cause most homebuyers to look at RFK’s Plan before looking at bank mortgages. (https://www.kennedy24.com/housing). As a result of RFK’s Plan, the effects of banks leaving the mortgage market would include a decline in competition in the mortgage market. (https://www.forbes.com/sites/qai/2023/01/11/wells-fargo-is-backing-out-of-the-mortgage-marketwhat-does-it-mean-for-homebuyers/?sh=58a8591537ca). This decline in competition would affect realtors and could cause it to be more difficult for homebuyers to get a mortgage Id.

Once in place, RFK’s Plan could cause an increase in home purchases, which could have the unintended effect of increasing housing prices. By encouraging more citizens to purchase homes, the cost of houses will also increase as the demand for houses become for common. (Goodman, Urban Institute). Naturally, as people are encouraged to participate in the housing market, the cost of houses will increase. Id.

Although RFK’s Plan sounds great on paper, it might have some legal complications competing with the existing agency mortgage loans and the FTC’s current regulations on mortgages. While the Plan’s attractive 3% interest rate is likely to incentivize home buyers, the unintended consequences on housing prices could counteract its positive effects. Additionally, if the Plan were implemented, it could become the standard mortgage that homebuyers would use, resulting in a government run monopoly on mortgages from banks’ inability to compete. Despite the appeal of government backed mortgages with low interest rates, much uncertainty still exists on the feasibility of RFK's Plan as it will have to face not only economic hurdles but legal ones as well.